![]() ISSN: 1885-8031

ISSN: 1885-8031

https://dx.doi.org/10.5209/REVE.79940

Crowdfunding para organizaciones de Economía Social: factores de éxito

Cinta Borrero-Domínguez[1]![]() ,

Encarnación Cordón-Lagares[2]

,

Encarnación Cordón-Lagares[2]![]() y Rocío Hernández-Garrido[3]

y Rocío Hernández-Garrido[3]![]()

Recibido: 24 de marzo de 2021 / Aceptado: 5 de enero de 2022 / Publicado: 31 de enero de 2022

Resumen. Este artículo tiene como objetivo analizar los factores clave de éxito del crowdfunding basado en recompensas en proyectos sociales impulsados por organizaciones de Economía Social. Para ello, utilizamos la información de la base de datos Goteo, que ha sido recopilada manualmente, y está formada por un total de 134 proyectos, que suponen alrededor de 12.321 decisiones de inversión y un importe total recaudado superior a un millón de euros. Utilizando el modelo logit, se han obtenido las siguientes conclusiones relevantes. En primer lugar, las variables que han mostrado un efecto positivo sobre las posibilidades de éxito de los proyectos de crowdfunding han sido las relacionadas con la experiencia de los fundadores y la ubicación del proyecto. En segundo lugar, en cuanto al tipo de entidad, las asociaciones tienen más éxito que las cooperativas, las organizaciones sin fines de lucro y las fundaciones. Finalmente, la variable relacionada con el género y el capital humano de los miembros del proyecto no influye en el éxito del proyecto.

Palabras clave: Crowdfunding social; Economía social; Recompensas; Emprendimiento; Entidades no lucrativas.

Claves Econlit: L31; B55; L26.

[en] Crowdfunding for Social Economy organisations: success factors

Abstract. This paper aims to analyse the key success factors of crowdfunding based on rewards in social projects promoted by Social Economy organisations. For this purpose, we used the information from the Goteo database, which has been compiled manually, and consists of a total of 134 projects, involving around 12,321 investment decisions and a total amount raised of more than one million euros. By using the logit model, the following relevant conclusions have been obtained. First, the variables that have shown a positive effect on the chance of success of crowdfunding projects have been those related to the experience of the founders and the location of the project. Second, regarding the type of entity, associations are more successful than cooperatives, non-profit organizations, and foundations. Finally, the variable related to gender and human capital of the project members don’t have an influence on the success of the project.

Keywords: Social Crowdfunding; Social Economy; Rewards; Entrepreneurship; Non-Profit.

Summary. 1. Introduction. 2. Theoretical Framework and hypotheses. 3. Methodology. 4. Findings. 5. Conclusions and future research. 6. References.

How to cite. Borrero-Domínguez, C.; Cordón-Lagares, E.; Hernández-Garrido, R. (2022) Crowdfunding for Social Economy organisations: success factors. REVESCO. Revista de Estudios Cooperativos, vol. 140, e79940. https://dx.doi.org/10.5209/reve.79940.

1. Introduction

The growth of Social Economy during the last decades has an important potential to create and develop jobs, promoting the search of strategies to drive different types of entrepreneurial initiatives, both in Spain and in Europe. This has led to the so-called "social entrepreneurship" that has grown dizzyingly, due to the demand to cover social needs (Sánchez, Martín, Bel & Lejarriaga, 2018) highlighting the creation of social value.

The most used definition of Social Economy is that included in the report prepared by Monzón & Chaves (2012:6) for the European Economic and Social Committee titled "The Social Economy in the European Union". According to this report, the Social Economy is defined as “the set of private, formally organised enterprises, with autonomy of decision and freedom of membership, created to meet their members’ needs through the market by producing goods and providing services, insurance, and finance, where decision-making and any distribution of profits or surpluses among the members are not directly linked to the capital or fees contributed by each member, each of whom has one vote. The Social Economy also includes private, formally-organised organisations with autonomy of decision and freedom of membership that produce non-market services for households and whose surpluses, if any, cannot be appropriated by the economic agents that create, control or finance them”.

In addition, the Social Economy has added a solidarity dimension by putting in place all kinds of governance schemes based on solidarity organisation and collective action, including, among others, funding modalities such as crowdfunding (Guttmann, 2021).

In recent years, Social Economy organisations have turned crowdfunding into a relevant source of project funding due to their need for resources, the decrease of public funding (Pape et al. 2019) and the reluctance of the financial sector to grant funding. Therefore, crowdfunding is an innovative financial source, which allows emerging entrepreneurial projects to raise funds from many people through Internet platforms (Ordanini, 2009; Agrawal, Catalini & Goldfarb, 2014; Mollick, 2014; Davies, 2014). This form of financing is expanding at a dizzying rate, captivating the attention of different agents, among which are entrepreneurs, businessmen and entities that have tried in one way or another to attract resources to undertake their projects (Short, Ketche, McKenny, Allison & Ireland, 2017).

In fact, crowdfunding platforms have arisen as a potentially important funding source for business and philanthropic initiatives. It has grown faster than other financial innovations (Rau, 2020) and has specialised in such a way that now they target specific sectors (Yu, Johnson, Lai, Cricelli & Fleming 2017).

This kind of research based on crowdfunding in Social Economy organisations has hardly been analysed by researchers. This is the reason for the novelty of this study, which represents a new contribution to improving their knowledge. The importance of people and their satisfaction over capital, helps to increase confidence in these Social Economy projects when collaborating in their funding. According to Rey-Martí, Mohedano-Suanes & Simón-Moya (2019), crowdfunding in the context of social entrepreneurship is possible because investors make their decisions based on the social and/or environmental impact of the projects they finance.

Crowdfunding allows investments to be made in financial benefits but also in social and environmental impacts and in personal interests (Baumgardner, Neufeld, Huang, Sondhi, Carlos & Talha 2017). Cecere, Le Guel & Rochelandet (2017) similarly found that prosocial drivers justify involvement in the campaign.

In fact, charities traditionally have depended on the campaigns run by donors who give small donations to fund their causes. The system was the same, but what is innovative is the global growth of crowdfunding platforms and the amount of funding they arise. Crowdfunding is now a global phenomenon that makes funding available in almost every single country in the world (Rau, 2020).

This paper analyses the factors that influence the success of crowdfunding projects promoted by Social Economy organisations, in one of the Spanish platforms, fostered by a non-profit foundation. Thus, being a foundation, the Goteo platform offers tax advantages to funders, allowing the tax relief of the amounts contributed, which can influence the success of the promoted projects. The need for this type of studies lies in the fact that, as pointed out by Zhou & Ye (2018) although many non-profit organizations have chosen the crowdfunding alternative because of its growing popularity, few entities have attempted to understand the systematics of this form of funding to develop strategies that will increase the success of campaign funding through this system.

The rest of the document is structured as follows: In the following section, we present the theoretical background and hypotheses. We then describe the data set and methodology. The findings and empirical evidence from our study are presented in the section below. And the final section summarizes our main findings and future research.

2. Theoretical Framework and hypotheses

The idea of crowdfunding is not new and began in offline environments (Gras, Nason, Lerman & Stellini, 2017). However, the Internet has extended the use of this alternative funding source, through multiple online platforms, which offer the four different ways of crowdfunding (donation, reward, loan, and investment) (Löher, Schneck & Werner, 2018). While lending and equity are considered investment models, reward and donation are seen as non-investment models (Schneor & Munim, 2019).

According to Kshetri (2015), together with other forms of fundraising activities, crowd based online technology for raising funds is considered a disruptive and innovative way of entrepreneurial financing.

The popularity of crowdfunding platforms is linked to their ease of use which has led to thousands of successful crowdfunding campaigns being completed in recent years (Koch & Siering, 2015).

This study analyses crowdfunding based on rewards, where individuals contribute to the financing of a project without receiving any type of financial incentive, return or reimbursement of the funds contributed. Instead, they receive a reward for supporting the project, which can range from acknowledgements for the amount donated to the delivery of the funded product or service, e.g., access to games, films, music (Chan, Park, Patel & Gomulya, 2018). Crowdfunding entails both complex and holistic relationships that cannot be understood from self-interest or altruistic perspectives (André, Bureau, Gautier & Rubel, 2017). If individuals know that their contribution will make an impact, they are more likely to support crowdfunding projects financially (Kuppuswamy & Bayus, 2017).

For their part, to ensure a feasible crowdfunding, entrepreneurs must provide a suitable environment for funders to make a return on their investment. The form and scope of the community benefits will determine the type of collective finance to be used by the entrepreneur (Belleflamme, Lambert & Schwienbacher, 2014). In this sense, it has been demonstrated that the motivation of investors depends on the type of crowdfunding (Cholakova & Clarysse, 2015). According to results higher success rates are linked to non-profit and charities rather than to for-profit ventures (Pitschner & Pitschner-Finn 2014).

The platform on which the crowdfunding takes place also has a key role. Although platforms can work with one or several crowdfunding models (donation, reward, loan, or capital), hybrid platforms are not abundant. Even if they are run by the same company, the most common is for each platform to focus on one crowdfunding model (Viotto, 2015).

Numerous variables that can influence the success of crowdfunding campaigns have been analysed in literature. Below is a brief review of the main variables used.

Project success

The dependent variable is a binary variable determined by the success of the project.

According to Skirnevskiy, Bendig & Brettel (2017), when a campaign ends, data on the amount of funds raised is collected and a dummy variable is generated to see the outcome of the campaign.

Thus, the project will be successful when reaching the minimum established funding (Lukkarinen, Teich, Wallenius & Wallenius, 2016; Kenost, 2016).

At Goteo.org, the minimum budget is "the capital necessary to carry out the initial, critical and essential tasks needed to start the project".

Gender

One of the variables analysed in the crowdfunding studies is gender, so Marom, Robb & Sade (2014) argue that projects promoted by women have higher success rates. In this sense, crowdfunding seems to reduce the problems that women have when accessing financing, since the traditional entry barriers are removed (Greenberg & Mollick, 2015). Moleskis, Alegre & Canela, (2018) argued that projects led by women have a higher probability of funding than projects led by men. For their part, Colombo, Franzoni & Rossi–Lamastra, (2015) argue that, on average, male promoters are less likely to receive support in terms of sponsorship and capital than women. In the same vain, Majumdar & Bose (2018), argued that since women are more likely trustable on crowdfunding platforms because they speak a more vibrant and optimistic language, including a wider range of people, they are more socially affiliated.

In contrast, Vismara (2016) showed that women show the same ability to attract funders but raise fewer funds. In this sense, Barasinska & Schäfer (2014) found no evidence that gender has any influence on whether a project is crowdfunded or not.

On the other hand, Greenberg & Mollick (2017) study this variable through homophily, defined as the tendency of individuals to associate with others based on shared characteristic. They use a new approach to funding called crowdfunding which reduces homophily, but does not eliminate it, in principle.

This reasoning leads to our first hypothesis:

– Hypothesis 1: The founders' gender has a positive effect on the likelihood of successful crowdfunding. Projects led by women borrowers have a higher success rate in financing than projects led by male borrowers.

Experience

On the other hand, experience is a widely analysed variable. Different studies show that if the campaign promoter has been successful in previous projects, potential funders will have more confidence in the project and in the promises of reward offered by the founder (Zheng, Li, Wu & Xu, 2014; Courtney, Dutta & Li 2017). Thus, the high participation of the project promoters in other crowdfunding campaigns indicates the experience of the sponsors (Wan, Luk, Fam, Wu & Chow, 2012). Thus, based on their previous experience, a promoter can identify factors that may influence the success of their campaign (Kunz, Bretschneider, Erler & Leimeister, 2017). Founders’ experience probably has a positive impact on the success of the funding, as during previous projects they can learn to make and present potentially successful projects and thus increase their chances of success (Janku & Kucerova, 2018). Therefore, entrepreneurs with more experience in financing will have a more precise understanding of why certain actions produce the desired results and which actions they don’t want to perform (Yang & Hahn, 2015). Success in crowdfunding can often be considered a long-term strategy (Hobbs, Grigore & Molesworth, 2016).

– Hypothesis 2: The past success of the founders increases the success rate of crowdfunding.

Human capital

Human capital is another highly qualified factor that can affect the success or failure of a campaign (Cha 2017) since it depends on the studies and training of the people promoting the projects. Funders frequently evaluate the human team to analyse the profitability of investing in a project (Franke, Gruber, Harhoff & Henkel, 2008; Cha, 2017). Furthermore, Ahlers, Cumming, Günther & Schweizer (2015) analyse how human capital in young ventures influence inexperienced investors to provide funds. Beckman, Burton & O'Reilly (2007) found consistent and often positive effects of human capital on the probability of start-ups to attract venture capital and going public.

According to Beier & Wagner (2014), projects presented in groups of people can take advantage, at their beginning, of the synergy of knowledge and skills from all the members of the project.

Therefore, human capital that makes up a project, is a crucial factor that influences its success. Starting projects with people without knowledge can be more difficult to continue (Cha, 2017) and to move forward.

– Hypothesis 3: The human capital of the founders has a positive influence on the likelihood of successful crowdfunding.

Location

Location can also play a key role in financing a project. Although crowdfunding platforms can mitigate effects related to geography, there are a significant number of studies that find a strong and relevant relationship with location (Agrawal, Catalini & Goldfarb, 2015; Lin & Viswanathan, 2016). In this sense, there are authors who have identified a "domestic bias" that explains the tendency of investors to finance locally based projects (Coval & Moskowitz, 1999; Lin &Viswanathan, 2013). Similarly, Josefy, Dean, Albert & Fitza (2017) argue that location plays an important role by promoting projects that share similar values with local communities. Therefore, if investors and project promoters share the same geographical area, the funding campaign is generally more financially supported (Agrawal, Catalini & Goldfarb, 2011). Besides, whether both parties feel a close geographical connection, it is more likely that projects are carried out more successfully (Lai & Teo, 2008; Strong & Xu, 2003).

The geographical affinity between investors and promoters, therefore, positively affects the fulfilment of the monetary objective of a crowdfunding campaign (Cha 2017) and thus its success (Knudsen, Florida, Gates & Stolarick, 2007) and Saxenian, 1996).

Burtch, Ghose & Wattal (2014) also find that lenders typically prefer borrowers who are socially proximate to themselves, in the sense that, they share a similar culture and are less geographically distant.

Mollick (2014) even found a significant relationship between geography and the proposed projects or campaigns with their success.

Geography is another important factor that influences the success of crowdfunding and the funds raised (Cha, 2017) because proximity to funders favourably affects obtaining capital for their development (Chen, Gompers, Kovner & Lerner, 2009; Stuart & Sorenson, 2003). However, crowdfunding campaigns are not limited to a specific geographic area (Agrawal et al., 2011; Stuart & Sorenson, 2003).

– Hypothesis 4: Founder location has a favourable impact on the probability of successful crowdfunding.

Type of Entity

Hörisch (2015) and Pitschner & Pitschner-Finn (2014) found that non-profit crowdfunding tends to be more successful than other projects with different organizational forms. In this regard, with this variable we try to analyse whether the type of non-profit entity has an influence on fundraising. Four types have been considered: cooperative, non-profit, foundation and associative entities.

In this sense, crowdfunding platforms increasingly host more projects that are proposed by companies belonging to the third sector (Michelucci & Rota, 2014) because they offer a diversification in financing plans, increasingly used by this type of entities (Phan, Bacq & Nordqvist, 2014). Therefore, crowdfunding is an essential tool to financially support projects (Michelucci & Rota, 2014) that could not be carried out with traditional financing mechanisms.

According to Pitschner & Pitschner-Finn (2014), projects promoted by non-profit entities receive more funds. Thus, they have a better chance of reaching the proposed minimum objective. However, they receive a smaller total monetary amount.

Furthermore, Belleflamme, Lambert & Schwienbacher (2013) state that non-profit projects are significantly more successful than others.

– Hypothesis 5: Associative entities are more likely to be successful in crowdfunding.

3. Methodology

3.1 Data and Method

Platform

The data used to conduct this study was taken from the Spanish crowdfunding platform Goteo. This is a collective financing platform for projects that offers individual rewards and generates collective returns.

In crowdfunding campaigns, a range of financing with a minimum and an optimum amount is established. In the Goteo platform, the optimum budget has to do with "additional tasks related to project development, sophistication, or improvement (increasing production, translating into other languages, offering it in other media, among others)". Also, some studies on reward-based crowdfunding indicate that projects with higher funding targets are negatively associated with success (Belleflamme et al., 2014; Cumming, Leboeuf & Schwienbacher,2020; Mollick, 2014; Zheng et al., 2014).

In Goteo the minimum budget has to do with "the capital necessary to develop the initial, critical and essential tasks to start the project". This amount makes it possible to determine the popularity of the campaign, since the percentage of the minimum target raised is visible on the campaign website at any time (Lukkarinen et al., 2016). However, none of the studies that include it in their analyses seem to show its possible connection to the success of the campaign (Ahlers et al., 2015; Ordanini, Miceli, Pizzetti & Parasuraman, 2011).

Unlike other platforms its projects are based on the philosophy of the common welfare and responds to the crowdfunding model "all or nothing", related to obtaining a minimum budget in 40 days, and if it is not reached all contributions are returned. In addition, if this minimum budget is reached during the first round of 40 days, a second round of the same duration can be started to reach the optimum budget.

Sample

The database includes information on 134 projects, which has been compiled manually. These 134 projects have resulted into more than one million euros raised and a total of 12,321 investment decisions. These projects have been promoted by associations, foundations, cooperatives, among others, between 2016 and 2018.

Our dependent variable is a binary variable determined by the success of the project. That means reaching the minimum established funding.

Our study has five independent variables. The variable that reflects the dominant gender of the members of the social crowdfunding project (GENDER) has been considered to analyse the existence of gender differences in the success of the project. Regarding the variable that gathers information on whether the founders have had previous successful collective financing experiences (EXPERIENCE), it is a question of verifying its impact on the success of the project. The human capital variable (HUMANCAPITAL) is used because, according to the literature, human capital attracts the attention of investors and facilitates access to finance. On the other hand, the location of a project (LOCATION) is also an important factor that can influence the results of the social crowdfunding project.

Regarding the variable representing the type of the entity, we have considered four types: cooperatives, non-profit organizations, foundations, and associations.

Table 1 shows the description of the variables used in this study, which aims to analyse the determinants that influence the success of crowdfunding projects.

Table. 1. Description of the analysed variables

|

Variable |

Description |

|

Dependent variable |

|

|

STATUSDUM |

=1 if the project is successful; =0 otherwise |

|

Independent variables |

|

|

GENDER |

=1 if all members of the project are women; =0 in another case |

|

EXPERIENCE |

=1 if project members have previous experience in similar projects; =0 in another case |

|

HUMANCAPITAL |

=1 if the members of the project have university studies; =0 in another case |

|

LOCATION |

=1 if the project is in Spain; =0 in another case |

|

ENTITY1 |

=1 if is cooperative entity; =0 in another case (reference category is associative entity) |

|

ENTITY2 |

=1 if is non-profit entity; =0 in another case (reference category is associative entity) |

|

ENTITY3 |

=1 if is foundation entity; =0 in another case (reference category is associative entity) |

Source: Elaborated by the authors.

3.2. Methodology

To achieve the proposed objective, the logit model is used in this study as a tool to analyse the existing relationship between a binary dependent variable, which is determined by the success or not of the project, and the information provided by a set of explanatory variables related to the characteristics of each project.

The estimation of the parameters in the model establishes the relationship of statistical dependence that exists between the explanatory variables X, relative to the characteristics of crowdfunding projects (see Table 1), and the probability that the binary dependent variable Y takes the value 1, in other words, that the project is successful or reaches the established minimum financing objective, adopting the following expression (McFadden, 1974):

(1)

(1)

where βi is the coefficient or parameter of the explanatory variables and X is the matrix of explanatory variables included in the model. The predicted probabilities are limited between 0 and 1.

Logit models are estimated using the maximum likelihood method. The sign of βi indicates the direction of the change in the probability of variations in the explanatory variables X. Thus, a positive coefficient βi would indicate that the probability of occurrence of the event increases, that is, the probability of the project being successful. Whereas a negative coefficient βi would show a decrease in the probability of the event occurring. In our case of dummy independent variables, the marginal effect is expressed in comparison to the base category (Xi=0).

On the other hand, the exponential of the parameter associated to the variable Xi, known as odds ratio or relative risk, is the amount by which the response advantage Y = 1 is multiplied when the value in Xi increases by one unit, with no change in the values of the rest of the explanatory variables. That is, a positive sign in the exponent causes an increase in the probability of occurrence of the event, a negative sign reduces this probability and a coefficient close to zero results in a value close to the unit, which practically does not affect the probability of occurrence of the event.

R-square of Cox-Snell and R-square of Nagelkerke are used to evaluate the overall fitting of the model. Thus, the Cox-Snell R-square or R2CS is given by

(2)

(2)

and the R-square of Nagelkerke by the following expression

4. Findings

Descriptive statistics

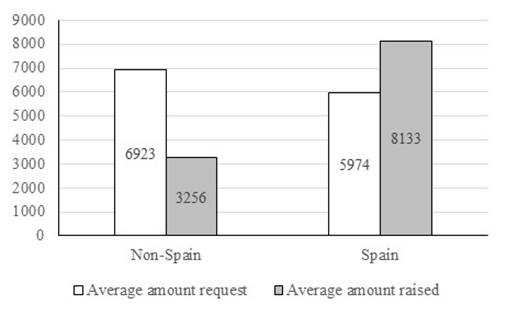

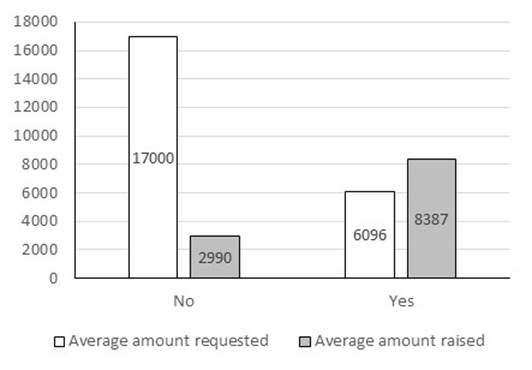

Figure 1 shows that while for projects located outside Spain the average amount raised is 53% lower than the average amount requested (minimum budget target), for projects located in Spain the average amount raised is 36% higher than the average amount requested. For its part, the test for equality of means confirms that, although there are no significant differences in the amount requested between projects located and not located in Spain (p-value 0.521), in the case of the amount raised the differences were significant based on that test (p-value 0.001). The Levene's Test for Equality of Variances has also been used.

Figure. 1. Average amount requested and raised (in euros) depending on whether the project is located or not in Spain

Source: Elaborated by the authors. Data collected from the Goteo platform.

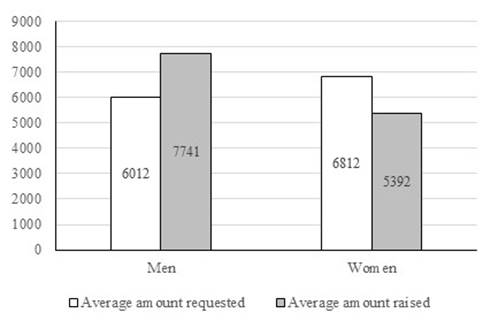

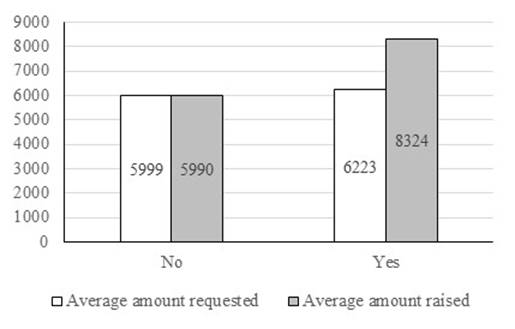

Although on average women request a slightly higher funding amount for their projects than men, the average amount raised by women was lower than that raised by men (Figure 2). However, based on the t-test for Equality of Means these differences were not significant in both the amount collected (p-value 0.440) and the amount requested (p-value 0.617) between men and women.

Figure. 2. Average amount requested and raised (in euros) according to the gender of the founders

Source: Elaborated by the authors. Data collected from the Goteo platform.

Figure 3 shows that while for projects whose founders do not have university studies, the average requested and raised practically coincide, in the case of projects whose founders have university studies, the average collected is 34% higher than the amount requested. On the other hand, based on the equality of means test, the differences were not significant either in the amount raised (p-value 0.838) or in the amount requested (p-value 0.263) between founders with university studies and those without.

Figure. 3. Average amount requested and raised (in euros) according to whether the founders have university studies.

Source: Elaborated by the authors. Data collected from the Goteo platform.

Finally, compared to the previous experience of founders in similar projects, Figure 4 shows that while for projects whose founders have no previous experience the average amount raised is 82% lower than the average amount requested, in the case of projects whose founders have previous experience the average amount raised is 38% higher than the amount requested. On the other hand, the mean equality test shows that there are no significant differences with respect to the amount collected for the two groups in question (p-value 0.771), but with respect to the amount requested there are significant variations at a 10% level of significance (p-value 0.067) in the case of founders with or without previous experience.

Figure. 4. Average amount requested and raised (in euros) according to whether the founders have previous experience or not

Source: Elaborated by the authors. Data collected from the Goteo platform.

Logit model

To know the determinants that may explain the success of social crowdfunding projects, the logit model of binary choice has been performed, with a dichotomous dependent variable, which allows us to classify projects according to whether the project is successful or not, that is, it reaches or does not reach the minimum financing objective established.

Table 2 shows the results of the estimated logit model with the variables that were found to be significant. In this sense, it is important to note the robustness of the model, as well as the absence of multicollinearity among the explanatory variables included in it. In fact, 90% of the observed cases turned out to be well classified based on our predictions (percentage accuracy in classification). Likewise, for this model the value of -2LL is 62.73. Moreover, the overall test for the model that includes the predictors, provides a chi-square value of 41.46, with a p-value below 0.0005, which indicates that our model fits significantly better than an empty model (i.e., a model with no predictors).

The R-square of Cox-Snell and R-square of Nagelkerke values are methods of calculating the explained variation. These values are sometimes referred to as pseudo-R-square values (and will have lower values than in multiple regression). Therefore, the explained variation in the dependent variable based on the model ranges from 23% to 44%, depending on whether you reference the R-square of Cox-Snell or R-square of Nagelkerke methods, respectively.

On the other hand, the Hosmer-Lemeshow tests the null hypothesis that predictions made by the model fit perfectly with observed group memberships. A chi-square statistic is computed comparing the observed frequencies with those expected under the linear model. A nonsignificant chi-square indicates that the data fit the model well (in our case, Chi-square of 5.405 and the p-value of 0.493).

The interpretation of the odds ratios shows how much the occurrence ratio of the event varies as a function of the change in the explanatory variables, that is, how much the success ratio of the project varies when the explanatory variable increases by one unit. Thus, when the odds ratios associated to a variable is greater than 1, the ratio increases when the value of the variable increases, as is the case of the variables HUMANCAPITAL, EXPERIENCE and LOCATION. Therefore, these variables have a positive effect on the occurrence probability of the event. On the contrary, when the Odds ratio associated to a variable is less than 1, the variable has a negative effect on the probability of event occurrence, as would be the case in the variables GENDER, ENTITY1, ENTITY2 and ENTITY3.

Table. 2. Estimated Logit model of binary choice

|

Variables |

Coefficients (b) |

Standard Error |

Wald |

P-value |

Exp (b) |

Hypotheses |

|

Constant |

-1.9975* |

1.1047 |

-1.8081 |

0.0706 |

0.136 |

|

|

GENDER |

-0.3564 |

0.9246 |

-0.3855 |

0.6999 |

0.700 |

H1 |

|

EXPERIENCE |

3.3538*** |

1.0764 |

3.1157 |

0.0018 |

28.612 |

H2 |

|

HUMANCAPITAL |

0.3068 |

0.7757 |

0.3955 |

0.6925 |

1.359 |

H3 |

|

LOCATION |

3.0796*** |

0.7760 |

3.9683 |

0.0001 |

21.749 |

H4 |

|

ENTITY1 |

-1.5505 |

0.9604 |

-1.6144 |

0.1064 |

0.212 |

H5 |

|

ENTITY2 |

-2.0166** |

0.9442 |

-2.1357 |

0.0327 |

0.133 |

|

|

ENTITY3 |

-2.3303** |

1.1073 |

-2.1045 |

0.0353 |

0.097 |

Note (*) (**) (***): Significant at a 10%, 5% and 1% level, respectively. R-square of Nagelkerke 0.439.

Source: Elaborated by the authors. Data collected from the Goteo platform.

Thus, the value 28.61 of the variable EXPERIENCE indicates that when project members have previous experience in similar projects, the reason why the crowdfunding project is successful, or in other words, that it reaches the minimum funding target is 28.61 times higher than when project members have no previous experience.

On the other hand, the value 21.7 associated to the variable LOCATION shows that when the project is in Spain the reason why the project is successful is 21.7 times higher than when the project is not located in Spain.

In the case of the variable related to entity (ENTITY1, ENTITY2 and ENTITY3), we observed that associative entities are more successful than cooperatives, non-profits, and foundations entities.

Finally, it has been verified that the variable related to gender (GENDER) and human capital of the project members (HUMANCAPITAL) have not been significant for the success of the crowdfunding project.

5. Conclusions and future research

In recent years, due to the economic and financial crisis and the reluctance of the financial sector to support and finance investment projects, a new way of raising resources known as crowdfunding has grown and has taken on an important role in financing social projects.

This study aims to contribute to the development of literature through the research of the determinants of success in reward-based crowdfunding projects within the field of Social Economy.

To analyse these determinants of the success of the social crowdfunding projects, we used data from the Goteo platform, which were collected manually, and carried out a logit regression model of binary choice.

Relevant conclusions of the analysis presented in this paper include the fact that, although women request on average a higher amount of funding for projects than men, the average amount raised for women is lower than for men. This reveals significant differences with respect to the amount raised according to the gender of the founders. The results also show that in the case of projects whose founders have university studies, the average amount collected is higher than the amount requested by the founders. This fact confirms the importance of human capital in attracting investors' attention and, therefore, facilitating access to financing.

On the other hand, regarding location, the results show that in projects located outside Spain, the average amount raised is lower than the average amount requested, whereas, for projects located in Spain, the average amount collected exceeds the average amount requested. This shows the important role that the location of the project plays in obtaining greater financing from locally based investors.

The logit regression model reveals that the variables related to gender (H1) and human capital of the project (H3) have not had an impact on the success of the crowdfunding project. On the other hand, the analysis has shown a positive effect on the success of the crowdfunding campaign have been those related to the experience of the founders and the location of the project. In fact, experience and localization have proved to be the variables that most influence the success of the project. Thus, with regards to experience, the results show that funders perceive projects whose founders have previous experience as more reliable, considering their previous capacity to develop a project and obtain successful results. The analysis clearly confirms the hypotheses that founders’ past success has a positive effect on the probability of successful crowdfunding (H2).

According to literature and H4, the results show that lenders typically prefer borrowers who are socially related to them. The reason could be that they share a similar culture and are less geographically distant.

On the other hand, with reference to H5, associative entities are more successful than cooperatives, non-profits, and foundations entities. Thus, it is observed that in this type of crowdfunding based on rewards, funders decide to invest in projects whose type of entity is associative.

The results of this study confirm the importance of analysing the factors that influence the success of this type of crowdfunding projects because of the significant investment decisions linked to this form of funding. The analysis of the determinants of success allows promoters and managers of the platforms to act according to those variables that attract the attention of funders, reducing the asymmetric information and enabling the achievement of the funding objectives.

In this sense, and despite the growing popularity of crowdfunding in the framework of business financing, research in the academic sphere is still in its early stages, which may be because few platforms have an enough number of projects for quantitative analysis (Vismara, 2016). In the case of this research, limitations have not been the scarcity of projects, but the lack of a database with the necessary information, which has led to manual data collection.

Moleskis et al. (2018) argued that through the theoretical and empirical findings of research streams on non-profit organisations and companies, their study helps us to better understand crowdfunding while incorporating a new analysis to the existing literature on this phenomenon.

In sum, it is necessary to continue moving forward in the analysis of the determinants of successful crowdfunding campaigns promoted by non-profit organisations, which find in this form of funding an alternative to undertake their projects.

We will study possible new variables based on the use of social networks (Facebook, Twitter, LinkedIn, etc) by project promoters that can influence whether a campaign is successful or not. In addition, further studies will use other variables to measure the projects' success. The limitations of our study are that it focuses on a single platform based on crowdfunding rewards. In the future, other platforms using other different crowdfunding modalities will be analysed for comparative studies.

6. References

Agrawal, A., Catalini, C., & Goldfarb, A. (2011) The geography of crowdfunding. The National Bureau of Economics Research. Retrieved from http://www.nber.org/papers/w16820.

Agrawal, A., Catalini, C., & Goldfarb, A. (2014) Some simple economics of crowdfunding. In J. Lerner, & S. Stern (Eds.), NBER book series: Innovation policy and the economy, 14(1), pp. 63-97. Chicago: University of Chicago Press.

Agrawal, A., Catalini, C., & Goldfarb. A. (2015) Crowdfunding: Geography, Social Networks, and the Timing of Investment Decisions. Journal of Economics & Management Strategy, 24 (2), pp. 253-274.

Ahlers, G.K.C., Cumming, D., Günther, C., & Schweizer, D. (2015) Signaling in equity crowdfunding. Entrepreneurship Theory and Practice, 39(4), pp. 955–980.

André, K., Bureau, S., Gautier, A., & Rubel, O. (2017) Beyond the Opposition Between Altruism and Self-interest: Reciprocal Giving in Reward-Based Crowdfunding. Journal of Business Ethics, 146 (2), pp. 313-332.

Barasinska, N., & Schäfer, D. (2014) Is Crowdfunding Different? Evidence on the Relation between Gender and Funding Success from a German Peer-to-Peer Lending Platform. German Economic Review, 15(4), pp. 436-452.

Baumgardner, T., Neufeld, C., Huang, P. C. T., Sondhi, T., Carlos, F., & Talha, M. A. (2017) Crowdfunding as a fast‐expanding market for the creation of capital and shared value. Thunderbird International Business Review, 59(1), pp. 115-126.

Beckman, C. M., Burton, M. D., & O'Reilly, C. (2007) Early teams: The impact of team demography on VC financing and going public. Journal of Business Venturing, 22(2), pp. 147-173.

Beier, M., & Wagner, K. (2014) Crowdfunding success of tourism projects: Evidence from Switzerland. Social Science Research Network. Retrieved 14/09/2021 from https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2520925.

Belleflamme, P., Lambert, T., & Schwienbacher, A. (2014) Crowdfunding: Tapping the right crowd. Journal of Business Venturing, 29(5), pp. 585-609.

Belleflamme P., Lambert T., & Schwienbacher A., (2013) Individual Crowdfunding Practices. Venture Capital: An International Journal of Entrepreneurial Finance, 15 (4), pp. 313-333.

Burtch, G., Ghose, A., & Wattal, S. (2014) Cultural differences and geography as determinants of online prosocial lending. MIS Quarterly, 38(3), pp. 773-794.

Cecere, G., Le Guel, F., & Rochelandet, F. (2017) Crowdfunding and social influence: an empirical investigation. Applied Economics, 49(57), pp. 5802-5813.

Cha, J. (2017) Crowdfunding for video games: factors that influence the success of and capital pledged for campaigns. The International Journal on Media Management, 19(3), pp. 240-259.

Chan, C. R., Park, H. D., Patel, P., & Gomulya, D. (2018) Reward-based crowdfunding success: decomposition of the project, product category, entrepreneur, and location effects. Venture Capital, 20(3), pp. 285-307.

Chen, H., Gompers, P., Kovner, A., & Lerner, J. (2009) Buy Local? The geography of successful and unsuccessful venture capital expansion. National Bureau of Economic Research. Retrieved 15/09/2021 from http://www.nber.org/papers/w15102.

Cholakova, M., & Clarysse, B. (2015) Does the possibility to make equity investments in crowdfunding projects crowd out reward–based investments? Entrepreneurship Theory and Practice, 39(1), pp. 145-172.

Colombo, M. G., Franzoni, C., & Rossi–Lamastra, C. (2015) Internal social capital and the attraction of early contributions in crowdfunding. Entrepreneurship Theory and Practice, 39(1), pp. 75-100.

Courtney, C., Dutta, S., & Li, Y. (2017) Resolving information asymmetry: Signaling, endorsement, and crowdfunding success. Entrepreneurship Theory and Practice, 41(2), pp. 265-290.

Coval, J. D., & Moskowitz, T. J. (1999) Home bias at home: Local equity preference in domestic portfolios. The Journal of Finance, 54(6), pp. 2045-2073.

Cumming, D. J., Leboeuf, G., & Schwienbacher, A. (2020) Crowdfunding models: Keep‐it‐all vs. all‐or‐nothing. Financial Management, 49(2), pp. 331-360.

Davies, R. (2014) Civic crowdfunding: participatory communities, entrepreneurs and the political economy of place. Entrepreneurs and the Political Economy of Place (May 9, 2014).

Franke, N., Gruber, M., Harhoff, D., & Henkel, J. (2008) Venture capitalists’ evaluations of start-up teams: Trade-offs, knock-out Criteria, and the impact of VC experience. Entrepreneurship, Theory and Practice, 32(3), pp. 459-483.

Gras, D., Nason, R. S., Lerman, M., & Stellini, M. (2017) Going Offline: Broadening Crowdfunding Research beyond the Online Context. Venture Capital, 19 (3), pp. 217–237.

Greenberg, J., & Mollick, E. (2015) Leaning in or Leaning On? Gender, Homophily, and Activism in Crowdfunding. In Academy of Management Proceedings: SSRN Electronic Journal.

Greenberg, J., & Mollick, E. (2017) Activist choice homophily and the crowdfunding of female founders. Administrative Science Quarterly, 62(2), pp. 341-374.

Guttmann A. (2021) Commons and cooperatives: A new governance of collective action. Annals of Public and Cooperative Economics, 92(1), pp. 33-53. https://doi.org/10.1111/apce.12291.

Hobbs, J., Grigore, G., & Molesworth, M. (2016) Success in the management of crowdfunding projects in the creative industries. Internet Research, 26, pp. 146–166.

Hörisch, J. (2015) Crowdfunding for environmental ventures: an empirical analysis of the influence of environmental orientation on the success of crowdfunding initiatives. Journal of Cleaner Production, 107, pp. 636-645.

Janků, J., & Kučerová, Z. (2018) Successful Crowdfunding Campaigns: The role of project specifics, competition and founders’ experience. Czech Journal of Economics and Finance, 68, pp. 351–73.

Josefy, M., Dean, T. J., Albert, L. S., & Fitza, M. A. (2017) The role of community in crowdfunding success: Evidence on cultural attributes in funding campaigns to “save the local theater”. Entrepreneurship Theory and Practice, 41(2), pp. 161-182.

Kenost, C. M. (2016) Crowdfunding: Is It a Viable Financial Model for Nonprofits? All Capstone Projects. Paper 231.

Knudsen, B., Florida, R., Gates, G., & Stolarick, K. (2007) Urban density, creativity, and innovation. Working paper. Retrieved 15/09/2021 from http://www.vwl.tuwien.ac.at/hanappi/AgeSo/rp/Knudsen_2007.pdf.

Koch, J. A., & Siering, M. (2015) Crowdfunding success factors: The characteristics of successfully funded projects on crowdfunding platforms. ECIS.

Kshetri, N. (2015) Success of crowd-based online technology in fundraising: An institutional perspective. Journal of International Management, 21(2), pp. 100-116.

Kunz, M. M., Bretschneider, U., Erler, M., & Leimeister, J. M. (2017) An empirical investigation of signaling in reward-based crowdfunding. Electronic Commerce Research, 17(3), pp. 425-461.

Kuppuswamy, V., & Bayus, B. L. (2017) Does my contribution to your crowdfunding project matter? Journal of Business Venturing, 32(1), pp. 72-89.

Lai, S., & Teo, M. (2008) Home‐biased analysts in emerging markets. Journal of Financial & Quantitative Analysis, 43(3), pp. 685-716.

Lin, M., & Viswanathan, S. (2013) Home bias in online investments: An empirical study of an online crowd funding market. Social Science Research Network. Retrieved 15/09/2021 from http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2219546.

Lin, M., & Viswanathan, S. (2016) Home Bias in Online Investments: An Empirical Study of an Online Crowdfunding Market. Management Science, 62 (5), pp. 1393–1414.

Löher, J., Schneck, S., & Werner, A. (2018) A research note on entrepreneurs’ financial commitment and crowdfunding success. Venture Capital, 20(3), pp. 309-322.

Lukkarinen, A., Teich, J. E., Wallenius, H., & Wallenius, J. (2016) Success drivers of online equity crowdfunding campaigns. Decision Support Systems, 87, pp. 26–38.

Majumdar, A., & Bose, I. (2018) My words for your pizza: An analysis of persuasive narratives in online crowdfunding. Information & Management, 55(6), pp. 781-794

Marom, D., Robb, A., & Sade, O. (2014) Gender dynamics in crowdfunding (kickstarter). SSRN Work. Pap, 2442954.

McFadden, D. (1974) Conditional logit analysis of qualitative choice behavior. In Frontiers in Econometrics, ed. Zarembka, New York: Academic Press, 105-142.

Michelucci, F. V., & Rota, F. S. (2014) The success of non-profit crowdfunding: First evidences from the Italian web-platforms. Torino: DIGEP—Dipartimento di Ingegneria Gestionale e della Produzione, Politecnico di Torino, 1-16.

Moleskis, M., Alegre,I., & Canela, M.A. (2018) Crowdfunding Entrepreneurial or Humanitarian Needs? The Influence of Signals and Biases on Decisions. Nonprofit and Voluntary Sector Quarterly, 1–20.

Mollick, E. (2014) The Dynamics of Crowdfunding: An Exploratory Study. Journal of Business Venturing, 29 (1), pp. 1-16.

Monzón, J. L., & Chaves, R. (2012) The social economy in the European Union. CIRIEC International, European Economic and Social Committee, Brussels.

Ordanini, A. (2009) Crowdfunding: customers as investors. The Wall Street Journal, 23(3), pp. 5-7.

Ordanini, A., Miceli, L., Pizzetti, M., & Parasuraman, A. (2011) Crowdfunding: transforming customers into investors through innovative service platforms. Journal of Service Management, 22 (4), pp. 443–470.

Phan P. H., Bacq S., & Nordqvist M. (2014) Theory and Empirical Research in Social Entrepreneurship, Northampton: Edward Elgar.

Pape, U., Brandsen, T., Pahl, J. B., Pieliński, B., Baturina, D., Brookes, N., & Zimmer, A. (2019) Changing Policy Environments in Europe and the Resilience of the Third Sector. Voluntas: International Journal of Voluntary and Nonprofit Organizations, pp. 1-12.

Pitschner, S., & Pitschner-Finn, S. (2014) Non-profit differentials in crowd-based financing: Evidence from 50,000 campaigns. Economics Letters, 123(3), pp. 391–394.

Rau, P. R. (2020) Law, trust, and the development of crowdfunding. Trust, and the Development of Crowdfunding (July 1, 2020).

Rey-Martí, A., Mohedano-Suanes, A., & Simón-Moya, V. (2019) Crowdfunding and social entrepreneurship: spotlight on intermediaries. Sustainability, 11 (4), 1175.

Sánchez Espada, J., Martín López, S., Bel Durán, P., & Lejarriaga Pérez de las Vacas, G. (2018) Educación y formación en emprendimiento social: características y creación de valor social sostenible en proyectos de emprendimiento social. REVESCO. Revista de Estudios Cooperativos, Tercer Cuatrimestre, Nº 129, pp. 16-38. DOI: 10.5209/reve.62492.

Saxenian, A. (1996) Regional advantage: Culture and competition in Silicon Valley and Route 128. Boston, MA: Harvard University Press.

Short, J., Ketche, D., McKenny, A., Allison, Th. & Ireland, D. (2017) Research on Crowdfunding: Reviewing the (Very Recent) past and Celebrating the Present. Entrepreneurship Theory and Practice, 41 (2), pp. 149-160.

Schneor, R., & Munim, Z.H. (2019) Reward crowdfunding contribution as planned behaviour: An extended framework. Journal of Business Research 103, pp. 56-70.

Skirnevskiy, V., Bendig, D., & Brettel, M. (2017) The influence of internal social capital on serial creators’ success in crowdfunding. Entrepreneurship Theory and Practice, 41(2), pp. 209-236. DOI:10.1111/etap.12272.

Strong, N., & Xu, X. (2003) Understanding the equity home bias: Evidence from survey data. The Review of Economics and Statistics, 85(2), pp. 307-312.

Stuart, T., & Sorenson, O. (2003) Liquidity events and the geographic distribution of entrepreneurial activity. Administrative Science Quarterly, 48(2), pp. 175-201.

Viotto, J. (2015) Competition and Regulation of Crowdfunding Platforms: A Two-sided Market Approach. Communications & Strategies, 99 (3), pp. 33-50.

Vismara, S. (2016) Equity retention and social network theory in equity crowdfunding. Small Business Economics, 46(4), pp. 579-590.

Wan, W. W. N., Luk, C.L., Fam, K.S., Wu, P., & Chow, C. W. C. (2012) Interpersonal relationship, service quality, seller expertise: How important are they to adolescent consumers? Psychology & Marketing, 29(5), pp. 365-377.

Yang, L., & Hahn, J. (2015) Learning from prior experience: an empirical study of serial entrepreneurs in IT-enabled crowdfunding. The 36th International Conference on Information Systems, Fort Worth, TX.

Yu, S., Johnson, S., Lai, C., Cricelli, A., & Fleming, L. (2017) Crowdfunding and regional entrepreneurial investment: an application of the CrowdBerkeley database. Research Policy, 46(10), pp. 1723-1737.

Zheng, H., Li, D., Wu, J., & Xu, Y. (2014) The role of multidimensional social capital in crowdfunding: a comparative study in China and US. Information Management, 51(4), pp. 488-496.

Zhou, H., & Ye, S. (2018) Legitimacy, Worthiness, and Social Network: An empirical study of the key factors influencing crowdfunding outcomes for non-profit projects. Voluntas: International Journal of Voluntary and Non-profit Organizations, 30(4), pp. 1-16.